Finance Act 2013 Changes to the 3-Year Tax Relief for Start-up Companies

Summary of Finance Act Changes

Finance Act 2013 (Section 34) provides for a significant enhancement of the tax relief for start-up companies by allowing any relief not availed of in the first 3 years of trading, due to losses or insufficiency of profits, to be carried forward for use in subsequent years. This is subject to the amount of relief in any year not exceeding the employer's PRSI contributions of the company, with relief for these contributions capped at €5,000 per employee and €40,000 in total for a year.

A 3-year tax relief for start-up companies commencing a new trade was introduced in 2009, and extended to end-2014, as a support to encourage new business development and employment creation. The relief, which is provided for under section 486C of the Taxes Consolidation Act 1997, is available where the total amount of corporation tax payable by the company for an accounting period falling within the 3-year start-up period does not exceed €40,000. Marginal relief is granted on a tapering basis where the total amount of corporation tax liability for the accounting period is between €40,000 and €60,000. To ensure that the measure is focused on job creation, the amount of tax relief is based on the employers’ PSRI contributions of the company in respect of its employees, subject to a limit of €5,000 per employee and an aggregate limit of €40,000 in any one period.

Prior to Finance Act 2013, the relief operated on a ‘use it or lose it’ basis. Relief was not available to a start-up company in any of the first 3 years of trading where a loss was incurred and relief was only partly available where the tax payable on profits from the new trade was not sufficient to enable the company to obtain full relief for its employer's PRSI contributions. There was no provision for carry forward of unused amounts to later years.

Section 34 addresses this limitation by allowing a start-up company, with eligible employer PRSI contributions in excess of the corporation tax referable to the qualifying trade1 for an accounting period within the 3-year start-up period, to carry forward the excess amount and use it to reduce corporation tax in respect of the trade in subsequent years. Provision is also made to enable a company entitled to marginal relief for an accounting period in the 3-year period to carry forward the additional amount of marginal relief that would have been available if the corporation tax in respect of the trade were of a sufficient amount to match the company's employer PRSI contributions.

Calculation of unused relief to be carried forward

Calculation of the amount of unused relief to be carried forward from the 3-year start-up period will depend on whether the company is eligible to claim full relief or marginal relief in any of the accounting periods in the 3-year period. The calculation of marginal relief is outlined in Appendix 2

In the case of a company eligible for full relief in an accounting period falling within the 3-year period2, where the total employer PRSI contribution exceeds the corporation tax referable to the qualifying trade for the accounting period, the excess amount (referred to in the legislation as a “first relevant amount”) is carried forward and will be available to reduce corporation tax referable to the trade in accounting periods following the 3-year period. For example, in the case of a company with a total employer PRSI contribution of €20,000 and corporation tax referable to the trade of €10,000 for an accounting period within the 3-year period, the company will be entitled to reduce that corporation tax to nil and to carry forward the unrelieved PRSI contribution of €10,000 for offset against corporation tax referable to the trade in accounting periods following the 3-year period3.

Use of carried forward relief in accounting periods following the 3-year period

Once the amount to be carried forward in respect of each accounting period within the 3-year period is determined4, these are then aggregated and that aggregate (referred to in the legislation as a “specified aggregate”) is then applied to reduce the corporation tax referable to the qualifying trade for accounting periods following the 3-year start-up period. This is subject to the requirement that corporation tax shall not be reduced in any accounting period by more than the total employer PRSI contribution for the accounting period.

Any residual amount of the specified aggregate that is not used in an accounting period can be carried forward and applied to reduce corporation tax referable to the trade in subsequent accounting periods until such time as the specified aggregate is fully used up. Thus, in the accounting period immediately following the 3-year start-up period, where the specified aggregate exceeds the amount by which corporation tax referable to the trade is reduced for that accounting period, the excess is carried forward and applied to reduce corporation tax referable to the trade for the next accounting period. Similarly, where it is not possible to fully use the excess in that accounting period, the remaining excess is, in turn, be applied to reduce the corporation tax referable to the trade for the succeeding accounting period and so on for each succeeding accounting period until there is no excess left.

An example of how the carry-forward provisions operate is provided in Appendix 1.

Commencement of new provisions

The Finance Act provisions will apply in respect of unrelieved amounts arising in accounting periods ending on or after 1 January 2013. This means that a company with an unrelieved amount of employer's PRSI in an accounting period (within the 3-year start-up period) ending in 2013 will be able to carry forward that amount and use it to reduce corporation tax referable to the qualifying trade in accounting periods following the 3-year period.

Accounting periods falling partly within the 3-year start-up period

Section 34 of the Finance Act 2013 also clarifies how the relief applies where part of an accounting period falls within the 3-year start-up period. Where a company carries on a qualifying trade in an accounting period falling partly within the 3-year period, that part of the accounting period is to be treated as a separate accounting period for the purposes of the relief. For example, where the 3-year period expires at the end of 2013 and the company's accounting period runs from 1 July 2013 to 30 June 2014, the six month period from 1 July – 31 December 2013 is treated as a separate accounting period and the corporation tax referable to income from the qualifying trade for this period, as well as the relevant employer PRSI limits, are determined by apportionment on a time basis.

Appendix I

Start-up company commencing a qualifying trade on 1/1/2013

Company eligible for full relief – i.e. total corporation tax liability does not exceed

€40,000 in any of the first 3 years.

Year |

2013 |

2014 |

2015 |

2016 |

2017 |

Trading Profits: |

14,000 |

12,000 |

70,000 |

100,000 |

120,000 |

Corporation tax [12.5%]: |

1,750 |

1,500 |

8,750 |

12,500 |

15,000 |

Employers PRSI contribution: |

10,000 |

10,000 |

10,000 |

10,000 |

10,000 |

Tax liability after s486C relief: NIL |

NIL |

NIL |

2,500* |

7,000 |

|

Unused amount carried forward: |

8,250 |

8,500 |

1,250 |

||

(‘First relevant amount’) |

|||||

Aggregate amount carried forward from 3 years: |

18,000 |

||||

(‘Specified Aggregate’) |

|||||

Relief claimed in years after 3 year period: |

10,000* |

8,000 |

|||

Aggregate amount remaining b/f to next year: |

8,000 |

NIL |

|||

*Relief cannot exceed total Employers’ PRSI contribution [€10,000] in this year. |

|||||

Appendix 2

Carry-forward of unused relief for a company entitled to marginal relief

A company with a total corporation tax liability of more than €40,000 but not more than €60,000 for an accounting period falling within the 3-year start-up period is eligible for marginal relief for the accounting period. In the case of a company on marginal relief, where the total employer PRSI contribution exceeds the corporation tax referable to the qualifying trade for the accounting period, an amount (referred to in the legislation as a ‘second relevant amount’) as determined by the marginal relief formula shall be carried forward and will be available to reduce corporation tax referable to the qualifying trade in accounting periods following the 3-year period. The amount to be carried forward is equivalent to the additional amount of marginal relief that would have been available to the company if its corporation tax in respect of the trade were of the same amount as its employer PRSI contribution.

There are three steps in calculating this amount:

(1) Step 1:- Calculate the actual amount of marginal relief available to the company for the accounting period. The amount of marginal relief available is the corporation tax referable to trade as reduced by the amount determined by the following formula:

where-

A + B the aggregate of (A) corporation tax referable to income from the qualifying trade and (B) corporation tax referable to chargeable gains on the disposal of relevant assets of the trade,

T is the total corporation tax payable by the company on all profits for the accounting period, and

M is the lower relevant maximum amount of €40,000.

(2) Step 2:- Calculate the amount of marginal relief that would have been available for the accounting period if the corporation tax referable to the qualifying trade were equal to the total employer PRSI contribution. The formula for determining this amount is as follows:

where-

C is the total employer PRSI contribution for the accounting period.

(3) Step 3:- Deduct the amount at (1) above from the amount at (2) to get the amount of marginal relief that is to be carried forward and applied to reduce corporation tax referable to the trade in accounting periods following the 3-year start-up period.

Example

The following is an example of how to calculate the amount of marginal relief to be carried forward from an accounting period falling within the 3-year start-up period.

Corporation tax payable and employers’ PRSI contributions for the accounting period are assumed to be as follows:

(€000's)

Total Corporation Tax (T) = 50

Corporation Tax referable to trade (A +B)5 = 20

Total employer PRSI contribution (C) = 30

Step 1 – Calculate the actual amount of marginal relief available for the accounting period:

This is the amount of corporation tax referable to trade (i.e. 20) as reduced by an amount determined by the formula:

where T = 50, M = 40 and (A + B) = 20

where T = 50, M = 40 and (A + B) = 20

i.e.

Thus, the actual amount of marginal relief available is: 20 – 12 = 8

Step 2 - Calculate the amount of marginal relief that would have been available for the accounting period if the corporation tax referable to the qualifying trade were equal to the total employer PRSI contribution:

The formula for determining this amount is as follows:

where C = 30, T = 50 and M = 40

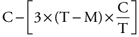

where C = 30, T = 50 and M = 40

i.e.

Step 3:- Subtract the amount calculated under Step 1 from the amount calculated under Step 2 to determine the amount of marginal relief to be carried forward:

Amount to be carried forward: 12 – 8 = 4 (i.e. €4,000)

Source: Revenue Commissioners. www.revenue.ie. Copyright Acknowledged

1. A qualifying trade is a new trade commenced in the period 1 January 2009–31 December 2014, which was not previously carried on by another person or the activities of which did not form part of another person's trade.

2. To be eligible for full relief, a company's total corporation tax liability must not exceed €40,000 for the accounting period.

3. An unrelieved PRSI amount arising in an accounting period within the first 3 years may only be used after the 3-year period, as the total amount of relief available for any accounting period cannot exceed the total employer PRSI contribution for the period.

4. This could include an amount of marginal relief if the company was eligible for marginal relief in an accounting period rather than full relief. Calculation of marginal relief is explained in Appendix 2.

5. i.e. the aggregate of corporation tax referable to income from the qualifying trade (A)and corporation tax referable to chargeable gains on the disposal of relevant assets of the trade